Ocean carriers likely to see $200 billion profits in 2022

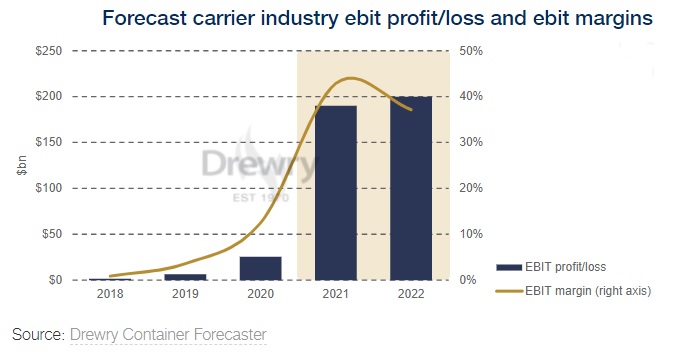

Ocean carriers are likely to report a combined profit of $200 billion (at a margin of 37 percent) in 2022 against the revised estimate of $190 billion in 2021, according to maritime consultancy Drewry in its latest Container Forecast report.

January 24, 2022: Ocean carriers are likely to report a combined profit of $200 billion (at a margin of 37 percent) in 2022 against the revised estimate of $190 billion in 2021, according to maritime consultancy Drewry in its latest Container Forecast report.

While Drewry feels 3Q21 probably represents the peak quarterly earnings for carriers, quarterly results in 2022 will stay on a more even keel that will average out slightly higher. "Our revised estimate for this year now stands at $200 billion (margin 37 percent).”

"The gravy train kept on rolling for ocean carriers in 3Q21 as the industry once again exceeded our expectations, posting an estimated EBIT performance of $70.9 billion, a staggering nine-fold improvement from $7.6 billion in the same quarter a year ago. Given that the industry was ahead of where we expected after nine months (estimated EBIT of $136.5 billion), Drewry had upgraded its annual forecast for 2021 from the previous guidance of $150 billion to $190 billion at a margin of approximately 43%."

So, what are the chances Drewy is likely to upgrade the 2022 earnings forecast? "Selfishly, I hope that we don’t have to upgrade as it will mean our forecast was accurate but the experience of last year makes me suspect there will be a need to adjust," says Simon Heaney, Senior Manager, Container Research Drewry. "Given the unpredictable nature of the market, I don’t want to say in which direction at this point."

See the numbers in this background: container demand growth losing momentum amid mounting headwinds, fast rising inflation, on-going supply chain bottlenecks and the Omicron Covid-19 variant slowing down the pace of growth in container handling.

Drewy has lowered its outlook for world port throughput in 2022 to 4.6 percent from the earlier 5.2 percent. The full-year 2021 estimate was also downgraded to 6.5 percent from 8.2 percent.

Drewry, however, feels carriers will ride a third year of 15 percent+ annual growth in total revenue. The earnings forecast rationale is based on the pivot from the volatile spot market to longer-term contracts “expected to be signed at much higher levels in upcoming negotiations. Carriers are building significant free cash flow that will give them ample room to allocate future income to dividends, pay down debt, and pursue growth opportunities."

Heaney added that Drewry expects spot freight rates to remain elevated but lower, on average, than last year. "More and higher contracts will pick up the slack. Overall, I do not expect to see the same extreme weekly variations as last year."

Bottomline: Drewry feels the majority of the risk from the highly unpredictable container market will reside with shippers in 2022 that is shaping up to be another year of severe disruption, under-supply and extreme cost.