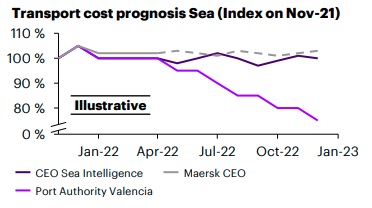

Supply chain crisis is here to stay till Q4 2022: Accenture

Low safety stock globally is fueling demand beyond Christmas, and full relaxation is not like before Q42022, consultancy firm Accenture said in its latest report.

November 11, 2021: Low safety stock globally is fueling demand beyond Christmas, and full relaxation is not like before Q42022, consultancy firm Accenture said in its latest report.

"Only moderate and long-term effects of short-term actions (e.g. U.S. government on port congestion, carriers ordering additional vessels) are likely," the report, Accenture Logistics Radar, said.

Accenture's suggestions include:

1. Identify short-term alternative transport modes (e.g. Coca-Cola using bulk transportation; rail freight from APAC)

2. Multi-echelon supply chain analysis and improvement to deliberately use existing inventory to increase supply chain output (reduce safety stocks)

3. Long-term planning with carriers and improvements of carrier structure (at least three global modes carriers with +20 percent transport volumes share); and

4. Improve existing supply chain forecasting and planning capabilities to sense demand fluctuation in advance.

In market-wise analysis, Accenture said APAC–Europe levels are at record-high (i.e. +500% in the last 12 months), capacity continues to be tight and equipment levels are insufficient in China and Vietnam.

Transit times for APAC–U.S has doubled (up to 36 days), and further congestion and capacity constraints are expected as congestions spill over. Voyages are being changed to minimise the effects of congestion (e.g. Hapag on port of Savannah).

Severe congestions have put the global sea freight market in imbalance, boosting rates and decreasing predictability. No major improvements are expected before Q12022.

Highlighting the key differences between the 2008 financial crisis and the current pandemic, Accenture said:

* Cash was missing in 2009, leading to demand decline; short-time work ensuring liquidity in 2021

* Strong recovery due to increasing commodities demand in Western countries (vs. reduced service demand) in 2021; and

* Constrained capacities not able to meet recovery in 2021; transport prices at record-high.

The pandemic-driven increase in spending on goods fuelled growth in ocean volumes and nearly uninterruptedly pushed container rates up since June 2020, according to Freightos, a digital booking platform for international shipping. "The additional demand driven by this year’s peak season supercharged pressure on rates this summer. This led to a 70 percent price spike over the last two weeks in July – the sharpest climb of the past 18 months. Now, the easing of that peak season demand – likely aided by the impact of energy-driven supply constraints to Chinese manufacturing – seems to have led to the largest price drop of the past two years."

Asia-North America West Coast rates fell 26 percent this week to $13,924/FEU. Rates are nearly 30 percent higher than their level just before the July spike, 261 percent higher than a year ago and 9X more than in November 2019.

Other trends like the recent dip in transpac vessel speeds on the return trip to Asia and falling container ship charter rates could also reflect a post-peak decrease in demand, Freightos added.